We have all heard the old saying, “Two things are guaranteed in life: 1. Death 2. Taxes.”

We are at an interesting time right now where prices of assets over the last 50+ years have seen a tremendous growth spurt. I always find it interesting talking to clients or other people in their 60s about income levels and prices of goods and services when they were younger.

Just last week, I was chatting with a client in his mid-60s who used to be a lawyer in a small town. He was telling me that when he started his career he made $30,000, and that was a very well-paying job at that time. Today, someone operating as a lawyer wouldn’t even get out of bed for that amount.

Inflation has been astounding.

One unfortunate outcome of growth is the taxes that inevitably need to be paid on assets. In particular one challenging situation that pops up its head is taxes concerning a family cottage.

When we die, we need to pay taxes. At death, all of our assets are said to be disposed of for tax purposes (called a deemed disposition), and if we can’t pay the income tax on those assets through our estate or other sources, the assets will be sold to cover the taxes. This often catches people by surprise and can cause a real point of contention if they are assets that we really want to keep in our family — for example, a family cottage.

All of us are allowed to have a principal residence in which we have to pay no income taxes on disposition, but sometimes people want to keep the cottage and their primary residence, or the growth on the principal residence outpaces the family cottage, so it makes sense to leave it designated as a principal residence.

I’m going to use a real-life example of how this tax burden can creep up on us.

Let’s use an example of a now 75-year-old female named Anna, who purchased a three-bedroom property in Toronto in 1964. Anna purchased this property for $25,000, and the current value is $1,500,000.

Anna also purchased a cottage in 1966 in cottage country for $12,000, which is currently worth $750,000.

Let’s project approximately what the tax burden on these properties would be.

Please note: We have assumed a top marginal tax rate in this scenario as this is the most common position.

Principal Residence Market Value = 1,500,000

Principal Residence Cost Base = $25,000

Capital Gain = $1,475,000

Taxable Capital Gain = $737,500

Personal Tax Burden (49.53% tax rate) = $365,284

Family Cottage Market Value = $750,000

Family Cottage Cost Base = $12,000

Capital Gain = $738,000

Taxable Capital Gain = $369,000

Personal Tax Burden = $182,766

Basically, if this family wants to keep the cottage upon Anna’s death, the estate of the holder would need to pay the Canada Revenue Agency $182,766, or they would need to sell the property to pay the income tax.

Remember that this person is currently only 75 years old; it’s not crazy to think that he could live for another 20 years.

So, from a financial planning standpoint, a few available options can help alleviate the pain of the tax burden.

Option 1: Transfer ownership today. This option would result in taxes payable today, but Anna’s tax burden would be finished. She could transfer ownership to a family member directly or to a family trust, for example. No matter what, this would result in tax payable today. (The above mentioned tax liability)

Option 2: Use life insurance to “buy money at a discount”. As you may be aware, life insurance is simply guaranteed tax-free money at a discount. This means that, no matter what, you should be able to use life insurance to guarantee that you pay less in premiums than you one day will inevitably claim. This benefit is also tax free.

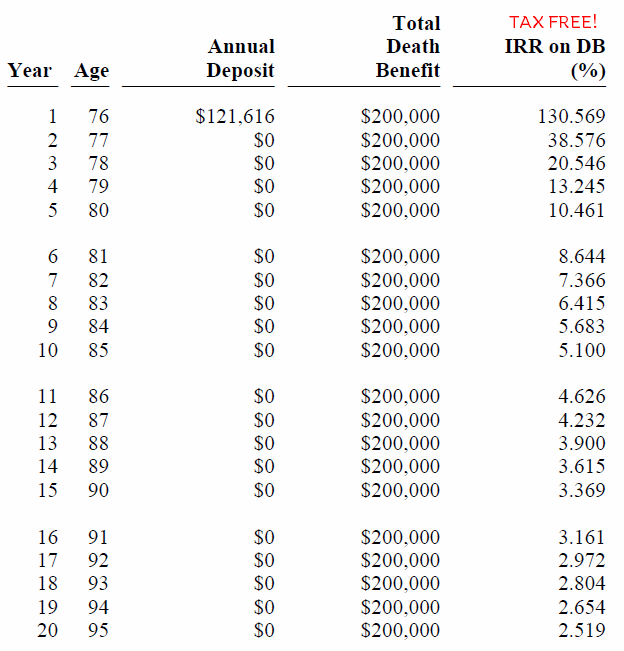

Using our above example, Anna would be able to purchase a $200,000 life insurance policy today for - $121,616. To simplify this post, I have assumed a one-time payment. This of course could be spread out over a different period of time is desired. I have included an illustration of this policy here;

Disclaimer: All information shown is taken from Manulife Illustration software. The projected interest rate used was 1.5% which is the guaranteed minimum interest rate on the long term portfolio.

Looking at the above illustration we see the cost/premium, coverage amount and the Internal Rate of Return (IRR). Remember the rate of return is tax free so basically you can multiply it by two to properly compare the investment to an RRSP or non-registered type account.

At age 95 to invest comparatively to this situation Anna would need to earn approximately a 5% rate of return before tax and remember this is guaranteed.

Another issue it that 1t age 75, in many cases our risk profile steers us away from being able to invest in much that offers that type of return.

When it comes to estate liquidation and estate tax, the other thing to be aware of is that all bank accounts and assets will also be charged with an estate tax called probate. This is a direct erosion of assets.

Basically, if you owe $200,000, you can either save up more than $200,000, have some of the funds absorbed by the government, or you can buy the $200,000 at a discount using life insurance.

Disclaimer: There is special tax treatment whereby we are able to use 1 year principal residence exemption on another property. For simplicity of this post I have left this out. To learn more about this calculation click here

---

Infinite Financial is an independently owned and operated Financial Services company in Barrie, Ontario. We specialize in Life Insurance, Retirement Planning and Estate Planning.

Our Certified Financial Planners represent the major Banks, Investment, and Life Insurance companies in Canada. We pride ourselves in offering advice independent of any particular Life Insurance, Bank or Investment firm and based strictly on client’s needs.

Contact us today or stop by our office in Barrie to say Hello!

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here